In today’s rapidly evolving energy landscape, Plug Power has emerged as a prominent player in the hydrogen industry.

1Q24 Review

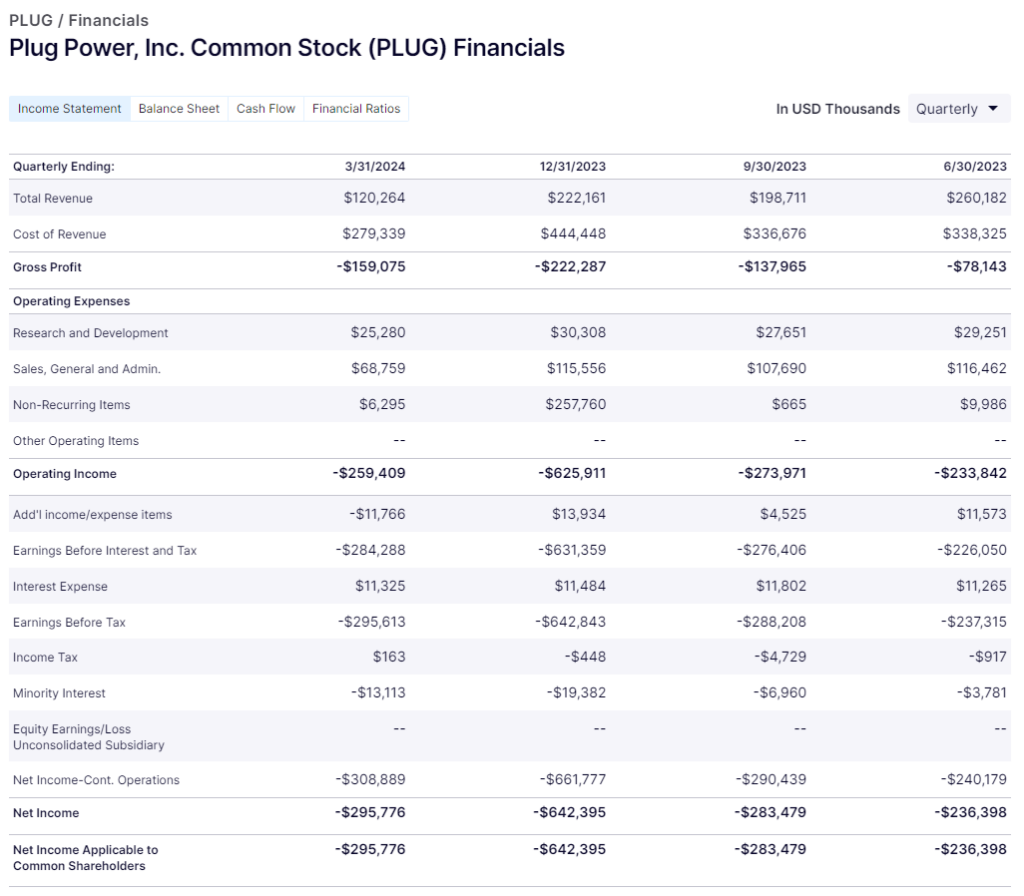

Plug Power’s first-quarter results painted a mixed picture, with both highs and lows. Despite being the largest hydrogen company in the US, Plug Power faced challenges, recording a revenue of $120 million, a sharp decline of 42.8% compared to the previous year. This decline in revenue was primarily driven by a decrease in sales volume, which fell short of market expectations.

Operating profit margin (OPM) took a significant hit, plummeting to -215.7%, a decrease of 115.9 percentage points compared to the previous year. This negative margin reflects the company’s struggle to maintain profitability amidst operational challenges. Additionally, earnings per share (EPS) dipped to -$0.46, missing consensus estimates by a wide margin.

Despite the bleak financial performance, Plug Power managed to mitigate some of the damage through cost-saving measures. Cash used for operations and capital expenditures decreased by 38% and 42%, respectively, indicating a proactive approach to financial management. The implementation of restructuring initiatives, price increases, and changes in contract structures contributed to this positive outcome.

The company’s decision to operate its own green hydrogen plants is a strategic move aimed at reducing reliance on external hydrogen suppliers. With plants operational in Georgia and Tennessee, and plans for additional capacity in Louisiana, Plug Power aims to enhance operational efficiency and drive long-term growth.

DOE Loan and Second-Half Expectations

While challenges persist, Plug Power is not without hope. The company is actively pursuing a Department of Energy (DOE) loan, with final results expected in the coming months. This loan could provide much-needed financial support and boost investor confidence.

Moreover, Plug Power anticipates a stronger performance in the second half of the year, driven by increased sales volume and the leverage effect of fixed costs. With two-thirds of annual revenue typically generated in the second half, the company is banking on a recovery to turn the tide.

Despite short-term challenges, Plug Power remains a key player in the hydrogen industry, poised for long-term success. The company’s commitment to innovation, cost efficiency, and strategic expansion positions it well for future growth.